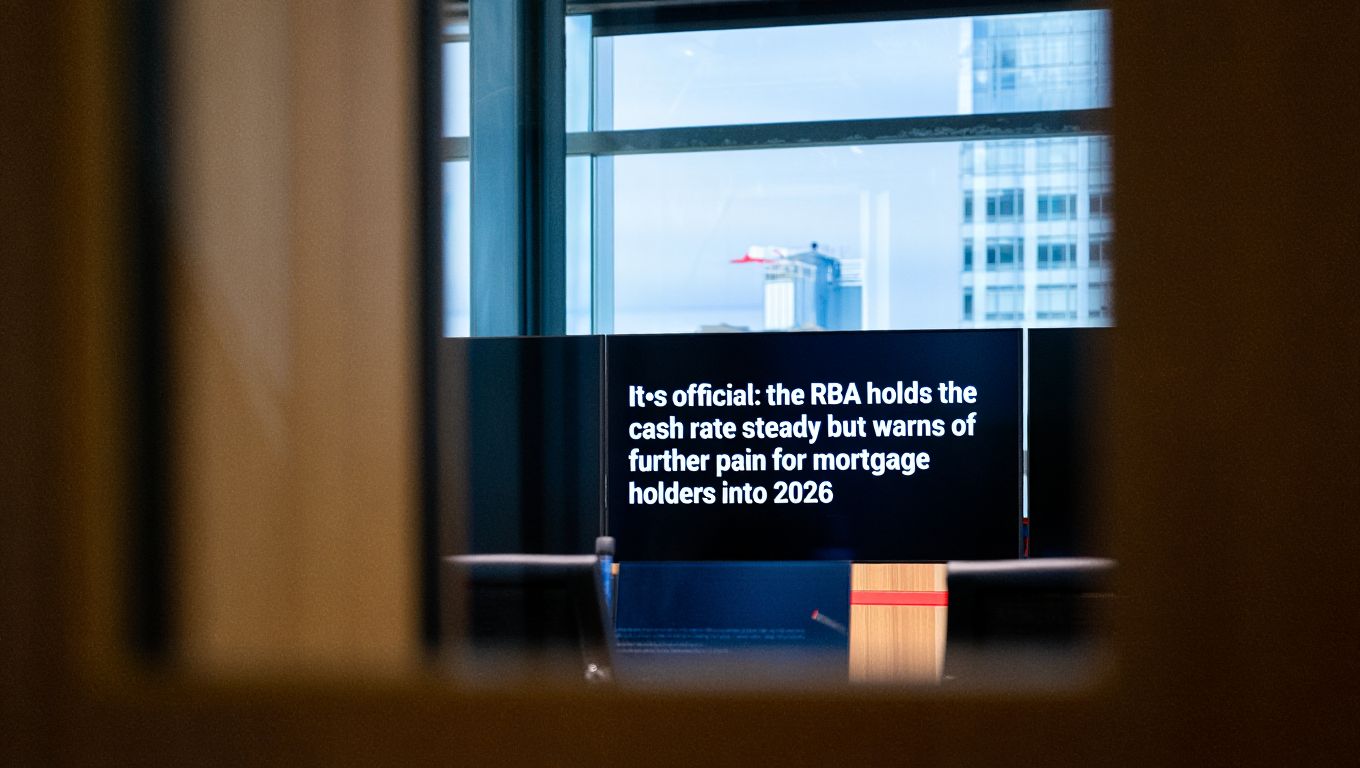

Households woke today to a familiar verdict from the central bank: rates are unchanged, but the pain is far from over. Markets had hoped for a hint of relief; instead, the message was clear — “higher for longer” still rules the day, and the squeeze on borrowers may linger well into 2026.

Why the pause isn’t a pivot

The decision to hold is less a change of direction than a check of instruments. Inflation is cooling, but the last mile — especially services — remains sticky. The bank wants evidence that price pressures are not just easing, but anchored, before it risks loosening the stance.

Officials nodded to global uncertainty, uneven growth, and a stubborn services impulse that feeds through to wages and local prices. In plain terms: “We’re not done yet.” Keeping rates steady buys time to watch how earlier tightening continues to bite.

Mortgage stress is becoming structural

For indebted households, this is the part that hurts. The fixed‑rate cliff may be less dramatic than last year, but the slow grind continues as more loans reprice at materially higher costs. Savings buffers, once ample, are thinning; discretionary spend is already pared back.

Arrears are still contained, yet the direction of travel is up. “The squeeze is real,” echoes through household budgets, where groceries, rent, insurance, and utilities have all jumped. With rates held, the monthly outflow stays heavy, and any calendar‑driven relief slides further into the future.

The economic trade‑offs the bank is weighing

The central bank is walking a razor’s edge: crush inflation without crushing jobs. A slower economy is by design, but the line between cooling and cracking is perilously thin. Unemployment is likely to edge higher, wage growth to moderate, and demand to remain subdued.

Officials see risks on both sides. Ease too soon, and inflation can re‑accelerate. Hold too long, and household stress can snowball into weaker consumption and rising arrears. The policy path is still “data‑dependent,” translating, roughly, to: if services inflation and inflation expectations behave, cuts can begin; if not, the wait lengthens.

What this signals for housing and credit

Property markets have shown resilience, but resilience isn’t immunity. Higher servicing costs limit what buyers can borrow, capping price momentum even where listings are tight. Investors face a spread of headwinds: elevated mortgage rates, rising costs, and uncertain tax settings, offset by strong rents and low vacancies.

Banks remain well‑capitalised, but credit appetite is cautious. Serviceability assessments — including buffers above current rates — keep a lid on new lending. Refinancing activity persists as borrowers chase any fractional saving, though the easy wins are largely gone.

How borrowers can steady the ship

For households staring down another long year, practical steps matter more than rhetoric:

- Audit monthly cashflow, prioritise needs over wants, and schedule bills to avoid spikes

- Call your lender for a rate review; compare options and consider a broker’s leverage

- Use offset/redraw facilities; even small extra repayments compound into real savings

- Explore temporary hardship programs early; they’re designed to prevent worse outcomes

- Consider measured income boosts — overtime, side gigs, or room rentals where feasible

“Don’t suffer in silence” is more than a platitude; early conversations expand your choices.

What could change the timeline

Two things would shorten the wait: a faster‑than‑expected drop in services inflation and clearer gains in productivity. Both would cool unit labour costs without relying on a deeper slowdown. A decisive global disinflation — think softer US growth, lower imported costs, and calmer energy markets — would also help.

On the flip side, sticky rents, insurance premiums, or renewed commodity spikes could keep headline inflation elevated. A tight domestic labour market, if it re‑tightens, would complicate the math and keep rates parked longer.

What to watch next

- Monthly inflation prints: services components and trimmed‑mean signals

- Labour market data: hours worked, under‑employment, and wage momentum

- Retail and household spending: signs of resilience versus forced cutbacks

- Arrears and hardship metrics: early indicators of financial strain

In the bank’s lexicon, the phrase “higher for longer” is slowly morphing into “high until convinced.” That conviction demands durable proof: inflation inside the target band, expectations well anchored, and no fresh surprises from abroad.

For now, the policy stance says: hold the line. For mortgage holders, the lived reality is: hold your nerve. Relief is still on the map, but the road to it runs through patience, planning, and relentless attention to the household bottom line.