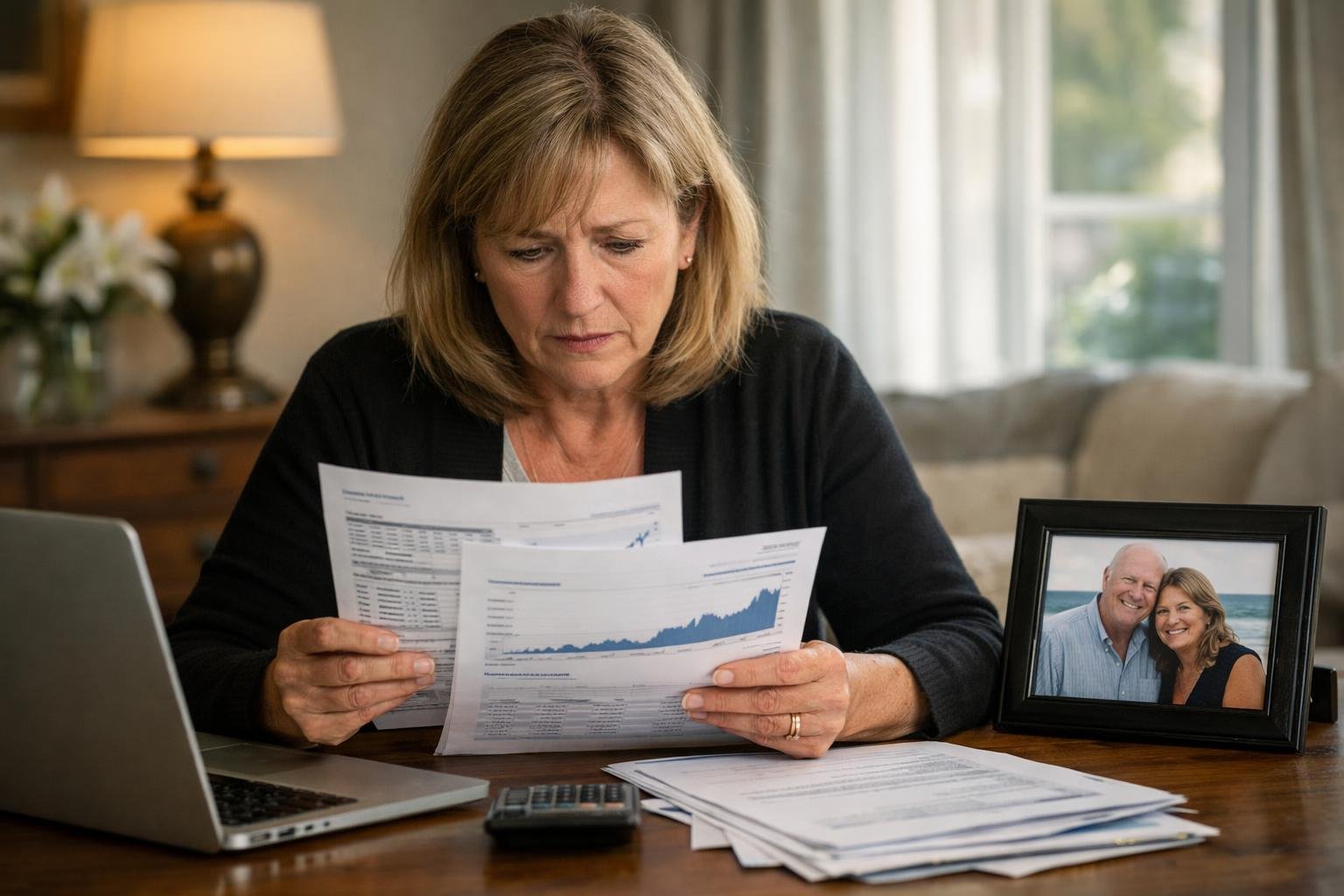

She found the statements in a faded folder at the back of a drawer—line after line of quiet purchases, small and steady. A widow on the Gold Coast, still learning the shape of her new life, realized her husband had been buying exchange-traded funds since 2001, without fanfare, without speeches. The account, now worth more than $1.1 million, felt like a message written over two decades: keep calm, keep going.

“He never bragged about money,” she said. “He just liked things that were simple and reliable.”

A quiet habit, two decades in the making

Every month or two, he’d buy a few more shares. Sometimes he’d add to a broad-market fund, sometimes to one focused on dividends, always with the same modest method. He didn’t chase headlines; he chased habits.

This wasn’t a tale of perfect timing or brilliant stock-picking. It was a story of minutes that turned into years, of routine contributions that became capital, of dividends quietly reinvested. The portfolio’s beauty came from its plainness: diversified ETFs, low fees, automatic reinvestment.

“He used to say, ‘Make a decision once, and let the system do the work.’” In a world that rewards the loud and the urgent, he built wealth with the soft and the slow.

The math of patience

ETFs are boring on purpose. They buy whole markets, accept average returns, and lower the chance of catastrophe. Over long horizons, average—when it’s low-cost and consistent—is often excellent. Add time and reinvested income, and the curve begins to bend.

The early 2000s brought a recession; 2008 was a storm; 2020 was a shock. He kept buying through all of it. That’s the essence of dollar-cost averaging: you buy when prices are high and when they’re low, letting volatility be a partner, not a threat. Over 20-plus years, the mix of contributions, dividends, and compound growth did what it usually does—it surprised the patient.

“He wasn’t trying to be clever,” she said. “He was trying to be consistent.”

- What made it work: low fees, broad diversification, regular contributions, reinvested dividends, and a refusal to panic.

Beyond the numbers

Grief has a rhythm. Some days you count papers, some days you count memories. The portfolio changed the math, but it also changed the tone. There was no lottery-like thrill, only a faint, sturdy reassurance—bills can be paid, grandkids can be helped, time can be bought back.

She noticed little clues he’d left: a list of logins, a note about beneficiaries, a reminder to keep costs down. It wasn’t secrecy; it was sparing her from worry. “He didn’t want money talk to feel like a burden,” she said. Now, with the dust settling, she sees it as a shared project that only reveals itself late.

The windfall is not a license to splurge. It’s a cushion with a purpose. She’s meeting a planner, updating wills, and learning how distributions and taxes work. Most of all, she’s setting a cadence she can keep—selling a little, rebalancing a little, donating a little. “He gave me a plan disguised as a garden,” she said. “Now I just have to water it.”

A nudge to the rest of us

Money secrets can be sweet, but they can also be stressful. If he had not kept records, the picture would be blurred. The quiet genius of his plan wasn’t just investing; it was leaving trails for the future. A simple folder. Clear labels. Fewer funds. Automatic everything.

There’s a lesson in the tempo: pick an allocation you can sleep with, automate your contributions, and ignore the daily chorus. Revisit once or twice a year. Adjust only when your life changes, not when the market throws a tantrum.

Another lesson: talk. Not about tickers, but about intentions. Where are the accounts? Who are the beneficiaries? What’s the plan if one person goes first? “It’s not morbid,” she said. “It’s merciful.”

And perhaps the sharpest point: you don’t need a perfect start. He began with small amounts, during imperfect times. The magic wasn’t the moment—it was the motion. Twenty years later, the line on the chart tells the story only numbers can tell, while the folder in the drawer tells the rest.

On the final page of his notes, a single sentence: “Slow is smooth, smooth is fast.” She read it twice, felt the room grow quiet, and smiled. The market had been working while they lived their lives. Now, the habit he built out of prudence has become her bridge to what comes next.