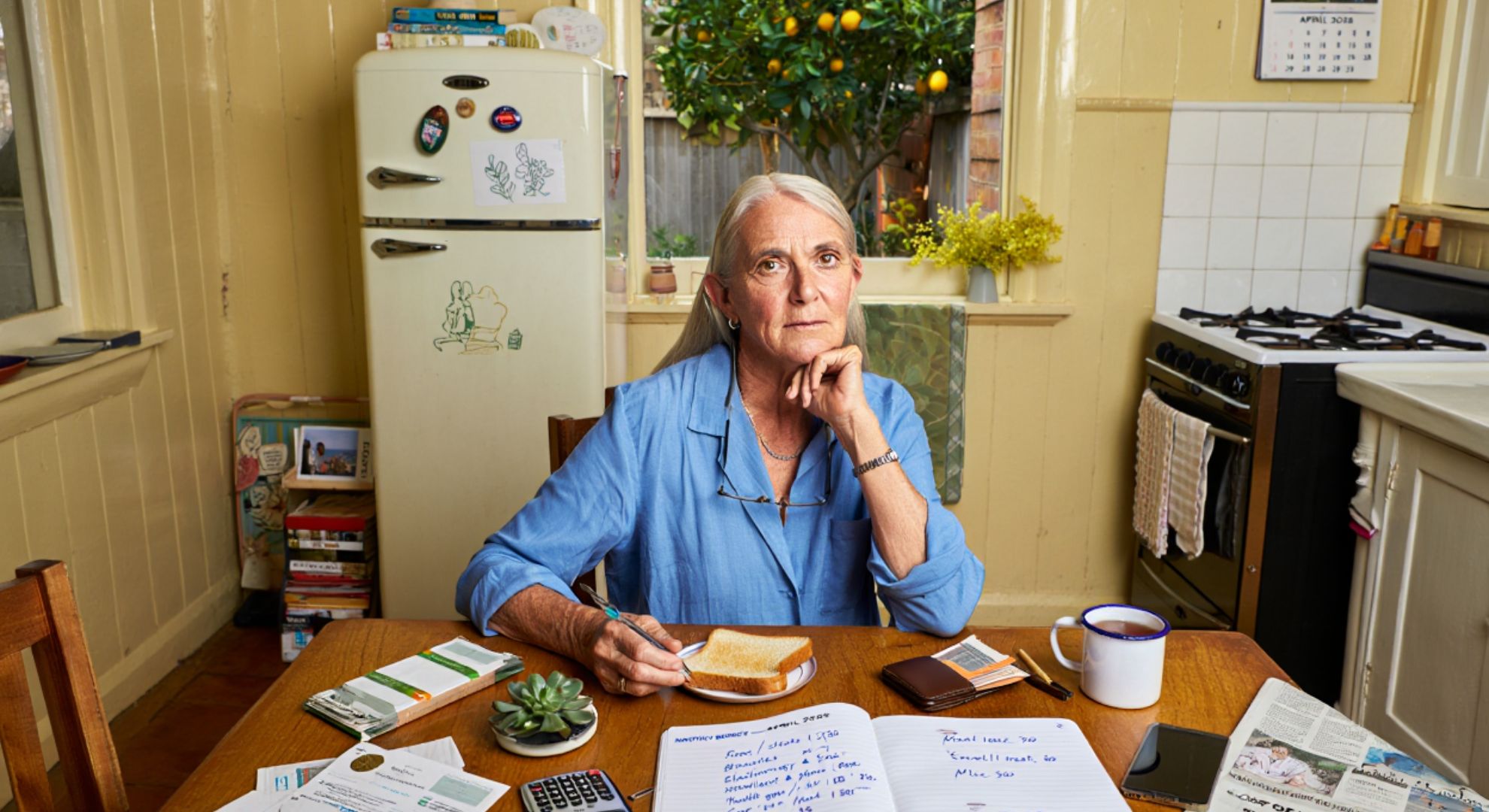

For many Australians, the retirement years arrive with both freedom and new financial realities. In 2026, the typical retiree is working with about $2,890 each month, a figure that reflects rising costs and shifting household patterns. Some call that budget “manageable,” while others say it’s “tight but livable,” depending on housing, health, and how confidently their savings are invested.

What sits inside that monthly figure

The monthly spend now stretches across a familiar mix of essentials and small comforts. Housing remains the chief divider between those who feel at ease and those who feel squeezed. Health outlays are steadier but stickier, and food costs remain a weekly reality no one can fully dodge.

“Every dollar needs a job, and every job needs a deadline,” as one retiree quipped while describing their routine bill calendar. That mindset captures how many now prioritise cashflow over grand, one-off savings wins.

Where the money usually goes

An indicative split shows how the average retiree might allocate limited funds, even as prices shift month to month:

- Housing and utilities: 30–35%; Food and groceries: 15–20%; Health and insurance: 15–18%; Transport: 8–12%; Communications and digital: 4–6%; Leisure, gifts, and travel: 8–12%; Contingency: 5–10%

This isn’t a rulebook, just a snapshot that helps people check whether any single cost is overheating. If two lines consistently bloat, many retirees trim discretionary spending first, then hunt for utility savings or health-plan tweaks.

Pension, super, and side income

For a large share of retirees, the Age Pension remains the cornerstone of monthly income, with indexation helping to cushion some inflation. Superannuation drawdowns add flexibility, especially for those comfortable with a conservative mix of assets that still aims for modest growth. A minority pick up casual or part-time gigs, not just for income, but for structure and social connection.

If you’re juggling these streams, the biggest gains often come from coordination: lining up pension dates, dividend timings, and bills to smooth the calendar. “When the bills land with the income, I sleep better,” said one reader who automated nearly everything to reduce surprises.

Homeowners versus renters

Nothing shapes retirement cashflow more than where and how you live. Mortgage-free homeowners often enjoy a wider buffer, using it for health, modest travel, or upgrades that cut future running costs. Renters, by contrast, can see half their budget swallowed by the roof over their head, especially in tight city markets.

Downsizing remains a powerful lever, but not always an easy one. Some fear transaction costs and leaving familiar neighbourhoods. Others embrace smaller, efficient homes that lower bills and free capital to reinforce their investment base.

Inflation’s lingering imprint

The pace of price rises cooled from its earlier peak, yet many line items remain elevated. Groceries have normalised in pockets, but special buys and seasonal swaps still matter. Energy bills stabilised for some, then spiked again for others depending on plan renewals and state-level settings. Insurance, meanwhile, climbed on rebuilding costs and climate risk, leaving many to reassess excesses and inclusions.

“I don’t chase the cheapest plan; I chase the best value,” noted one retiree who renegotiates annually, switching only when the terms and the service both stack up.

Stretching each dollar further

Small moves compound into real relief. Concessions on transport, energy, and rates remain underused, and switching providers can reset baseline costs. Bulk-billing clinics and PBS safety nets help keep health expenses predictable, while preventative check-ups often save money before conditions escalate.

Food-wise, retirees praise batch cooking, freezer discipline, and a short list of high-rotation meals that are cheap, nutritious, and enjoyable. Travel remains possible with off-peak timing, seniors discounts, and flexible itineraries that avoid premium windows.

Mindset, not just mechanics

Two retirees with the same income can feel very different about money. The difference often lies in clarity and cadence: a tight but transparent plan calms the nerves, while a vague plan fuels anxiety. “I give every dollar a destination, then let the system run,” said another reader who treats their budget like a quiet appliance in the corner.

The other driver is community. Sharing tips, swapping referrals, and comparing bills with peers often surfaces better options faster than solo research. A five-minute chat can be worth a year’s worth of small cuts.

The bigger picture for 2026

A monthly target near $2,890 won’t fit every household, but it anchors the current conversation. Those below it can still feel secure with low housing costs and stable health; those above it may still feel pinched if rent or insurance rises keep biting. The goal isn’t a perfect number, but a living plan that adapts when prices move and life, inevitably, changes.

For many, the path forward is practical: know your essentials, trim the friction, automate what you can, and keep one eye on value, not just price. With that, the average month becomes less a juggling act and more a rhythm—steady, sustainable, and still open to a little joy.